Three Brain-dead Simple Ways to Make Money in a Down Market

I’ve been receiving a lot of concerns about the possibility of a stock market crash hitting the market.

That’s because there are a lot of threats in the market right now…

The Chinese economy possibly triggering a widespread financial crisis because of the failure of Evergrande (which I discussed here)... the Federal Reserve Bank tapering its asset purchases (which I discussed here)... the fear of high inflation (which I discussed here and here).

Folks are especially concerned because September 2021 is one of the rare months where the S&P 500 — an index used as a benchmark of the whole market — hit an all-time high and still ended the month down -4.76%.

We’ve seen a similar pattern in the Nasdaq, which went down -5.31% in September.

Folks want to know…

Is this the beginning of a downturn?

Listen, I haven’t been shy about my belief that we’re going to see below average market returns over the next few years. (See here.)

“Below average,” though, is not “negative.”

I can only tell you what we’ve seen in the past…

And draw conclusions from there.

What have we seen in the past?

Well, the Fed hasn’t turned off the spigot of free money floating in the economy and financial markets.

So long as the Fed is propping up the market, I have no reason to believe that there will be a prolonged downturn in stocks.

Something calamitous would need to happen.

And if there’s a crash, it will resemble March 2020, December 2018, and August 2015: a sharp downturn, a few months of choppiness, and a quick recovery.

For that reason, I’m currently looking at this September downturn as a healthy cooldown period, and an opportunity to invest cautiously.

Historical data supports this approach.

In the past 20 years (240 months), the S&P 500 has had 85 down months. 68 of those months, the S&P 500 was down more than 1%.

Now, had you invested the same amount in a mutual fund or ETF that tracked the S&P 500 every time there was a drop deeper than -1%...

Once you factor in dividends and capital gains and compounding (I’m using the S&P 500 Total Return Index for this)…

You would have seen an average return of 309.5% on your investments.

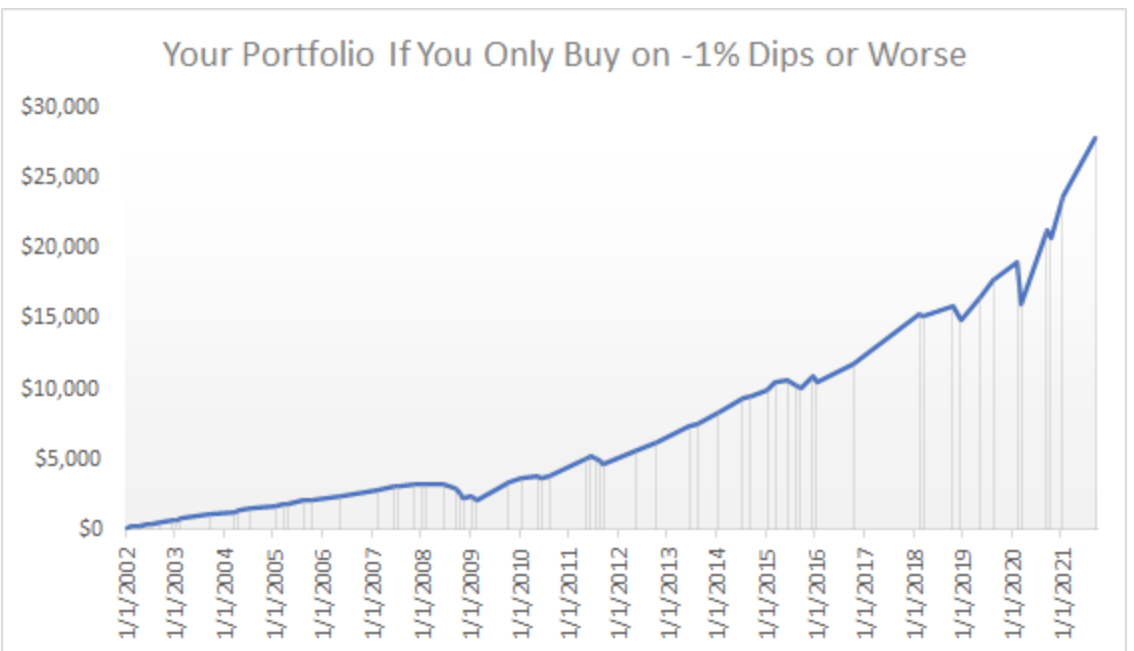

This is what your portfolio would look like if you only invested $100 every time this happened over the last 20 years (the lines indicate when you would have invested):

You would have cumulatively invested $6,800…

And that would have turned into $27,848 by now.

Here’s something you’re going to see me say a lot…

Downturns can be opportunities.

Not all downturns are opportunities, mind you. For instance, you don’t want to throw money at a penny stock going bankrupt after it’s fallen -95%.

But if you have a portfolio of good stocks with a history of surviving and thriving during downturns—companies that make money, have good growth prospects, and reward shareholders…

Or if you just invest in an index fund…

A price dip is an opportunity to invest more, rather than a signal to sell.

But here’s something else important I want to illustrate for you…

What happens if you just invest the same amount at the same time every month, regardless of what happens to the price of the S&P 500?

This strategy is called “dollar-cost averaging.”

Let’s say you invest $28.33 each month (that’s $6,800 divided by 240 months).

This is what your portfolio would have done:

You would have cumulatively invested $6,800…

And that would have turned into $25,242 by now. A 271.2% total return.

As you can see…

Investing on dips beats investing the same amount each month.

Those moments where you would have been most afraid to invest more money…

Were EXACTLY the moments where you should have invested more.

But let me show you what happens when we combine both strategies.

What happens if you invest $25 each month… And invest $100 whenever there’s a dip deeper than -1%?

You might think this strategy wins, but take a look:

Over the last 20 years, you would have invested $10,975 total…

And this would have grown to $42,957—a 291.4% gain.

That’s better than cost averaging, but a worse return than buying on dips.

Why?

Because sometimes the market is overvalued, and in those situations, if you invest, your average return will be worse over time.

“SO HOW DO I PROFIT IF WE’RE HEADING TOWARD A CRASH?”

The reason why “investing the same amount each month” and “buying on dips” both work is for two reasons…

They allow your money to compound and grow over time…

And they’re simple.

You never have to worry about making decisions.

You should also notice that the difference between strategies is pretty small if we’re talking about 20 years: 271% vs. 291% vs. 309%.

If you want to profit long term, it doesn’t matter what you do, so long as you’re investing.

But the point of this exercise is to illustrate that if you invest every time the market experiences a significant monthly decline...

Over time, you’ll be fine.

Don’t be afraid. Be intelligently opportunistic.

I have suspected that the market entered “bubble territory” beginning in September 2020 and stopped investing in May 2021.

For that reason, I have not been buying anything in my own accounts.

That is, until this September dip. I invested a small amount of the cash I’ve put aside for long-term investing.

And if we see another decline during October?

I plan to invest a little bit more.

You should consider doing the same.