Should You Buy Gold Before the 2023 Recession?

There’s nothing quite like the feeling of holding a gold bar or a tall stack of gold bullion coins.

Gold, for good reason, has served as a marker for wealth and opulence for centuries.

But following the terrible bear market in stocks and bonds in 2022, and considering that many economists are predicting an economic recession in 2023…

Many investors and wealth builders are finding themselves wondering: “Should I invest in gold before a recession?”

There are reasons for buying gold and precious metals more broadly, as a way of diversifying your assets. But there are also many good reasons to avoid gold.

So let’s mine what we know for insights about how you can use gold to help you build wealth.

I’ll cover the case for gold and why it is often touted as a good investment and a fantastic hedge that can protect you against both market downturns and geopolitical threats…

And in the interest of being unbiased, I’ll cover why gold might be a bad investment for some (and, indeed, possibly most) prospective investors.

Then I’ll explain why, in 2023, gold looks like it might be a compelling speculation or trade.

Let’s get started…

Should You Buy Gold Before the Recession?

Video Summary:

In this video, we explore the pros and cons of investing in gold to help you make an informed decision.

I'll also explain the two macroeconomic catalysts that spurred me to invest in gold and silver—both in physical gold, like bullion coins and ingots, and some stocks.

Contents:

0:00 Intro

1:56 The Case for Gold: Why people love it so much

4:30 The Case for Gold: Tangibility

5:24 The Case for Gold: Portability

5:49 The Case for Gold: Privacy

6:20 The Case for Gold: Gold might have intrinsic value for nerdy reasons

7:10 The Anti-Gold Camp: Why most of the arguments in favor of gold are BS

8:10 Gold just isn't a very good long-term investment

9:43 Why I'm investing in Gold now: 2 catalysts

11:50 Will Gold actually protect you during recessions?

The Investment Case for Gold

It may surprise you to know that gold is not the oldest or longest lasting form of money. That accolade is reserved for “livestock.”

Nor is gold the first form of metal money (that one goes to bronze and copper).

Gold coins first circulated as an official means of exchange around 500BC, depending on your source.

When metal money hit the scene — bronze and copper coins included — it caught on quickly. For the first time, people could pay for things by count, instead of by weight.

But since silver tarnishes over time, and bronze isn’t considered a “rare” enough metal for controlled coinage…

Gold became the preferred form of currency.

Gold is thus the “original and best money,” the goldbugs assert.

For one, it’s a rare enough metal — such that not everyone can mint gold coins in their basement.

Yet it wasn’t so rare that it was hard to find and create enough coins for circulation.

And when compared to paper or fiat money, which first appeared in China in the 11th century, gold certainly has added benefits.

[Fiat currency is any government-issued money that is not backed by a commodity like gold or silver.]

For example, while any government can print more money, no one can print more gold. Gold must be discovered, mined, stored and physically transferred, and minted.

And up until 1971, the amount of paper money circulating in the U.S. economy was directly pegged to the amount of physical gold stored by the Federal Reserve.

If you’ve ever heard of “the gold standard,” this is what folks are referring to.

But as soon as this link was severed, paper money printing soared… crushing the purchasing power of the U.S. Dollar by as much as 85%. Making paper money even more worthless today than it was. (Another argument in favor of gold’s supremacy.)

To this day, gold is seen less as a form of currency and more as a store of wealth.

In fact, after being net sellers of it for nearly a decade back in 2010, central banks began hoarding gold again…

In 2008, the spot price of gold broke $1,000 per ounce for the first time ever.

It crashed to $692.50 later that year.

Central banks love these corrections. It lets them buy gold at cheaper prices.

And in fact, according to the World Gold Council, central banks are gobbling up gold at levels not seen since 1967. Much of this part of a global “flight to safe assets” due to ongoing fears of inflation and a looming recession.

Many pessimistic investors are following suit and buying gold for three big reasons: It is tangible. It is portable. And in most cases, it’s private.

Let’s go over each of these characteristics quickly:

Gold is Tangible:

Your stocks and bonds exist on an electronic spreadsheet, as does the money in your bank account. This spreadsheet is the property of some huge financial institution. What if it disappeared?

It’s not likely, but it’s still a possibility. Global banks have failed. They’ve shut their doors and put limits on withdrawals to prevent crazy bank-runs that could lead to bank failures. Hackers can enter internal banking systems and drain accounts. These things have happened in recent history and happen every day to citizens worldwide.

Gold, on the other hand, can be physically held. While it can be stolen from its physical location, it’s a real and hard asset, unlike 1s and 0s on a digital ledger.

Gold is Portable:

Real estate is another tangible asset. But real estate is not portable. If, for some reason, you want to get out of the country, you can’t load up your property in your luggage and take it with you. You can take your gold with you. And since real estate is non-portable, you can’t protect it from confiscation, either. Hardworking people have lost their homes to fraud. One day they owned them, and the next day they didn’t.

Gold is Private:

Money in your bank account is not private. The banking system sees it. The government sees it. Who knows who else can see it. And the other problem with real estate (and many other forms of tangible wealth) is that it is actually public. Clerks record and preserve every real estate transaction you make for anyone to see. With a working knowledge of Google, your neighbors can study your real estate and what you paid for it. None of these problems exist with the gold bullion coins like Eagles, Maples, or Krugerrands.

These are the main benefits of owning gold. (It’s also divisible and scarce, two added perks we covered earlier. Another common quality we often see is its durability. Compared to paper, for example, it’s a lot harder to destroy.)

However, there is a slightly nerdier, final argument on gold’s behalf that I appreciate…

Gold has Intrinsic Value:

While many people have the opinion that gold and precious metals have intrinsic value, there might also be a logical argument for its inherent worth.

This argument is well stated by the economist and futurist George Gilder, who views wealth and knowledge to be one and the same.

If wealth is knowledge, then growth is learning. As he writes in his short book, The 21st Century Case for Gold:

Money is the channel that carries the information to investors, workers, small businessmen, major corporations and entrepreneurs. All need to gauge the success or failure of their attempts at growth… The source of the value of money is time — irreversible, inexorably scarce, impossible to hoard or steal, distributed with remorseless equality to rich and poor alike. As an index of time, gold imparts the accurate price signals needed for sustained economic growth and expanded opportunity.

The argument here is that, since money is information, governments only have the ability to increase the volume of money. But they ultimately have no ability to enhance the value of money.

Without that quality of time-bounded scarcity, free-floating currencies not backed by tangible assets fail everyone in an economy.

This argument gets, uh, far more into the weeds than we have the page space for here.

But for all intents and purposes, gold (or some kind of digital currency) shields money from manipulation and prevents some of the most egregious problems that arise from current monetary policies.

This covers the basis of the Pro Gold Camp well enough. How about the opposition?

The Case Against Gold as an Investment

All of the arguments about gold’s scarcity and serving as a tangible, portable substitute for money are, well, quaint.

At the end of the day, we’re talking about shiny rocks that aren’t especially industrially useful. (This is especially true for gold, but it might be a different story for silver, palladium, and platinum.)

Meanwhile, while gold is technically portable, it’s not easily portable.

It’s inconvenient if not impossible to carry a sizable gold cache around the world. In the modern world, there are customs agents to navigate. There’s the sheer heft of it — gold (especially gold bars) is not light.

Gold is considered durable, but it’s not indestructible. And in fact, with gold being very malleable, wear and tear through exchange and use over time does lead to the lowering of gold in coins over time. The more worn they are, the less valuable collectible gold coins are.

Sure, gold is divisible. But again — not easily. It requires specialty equipment and extreme temperatures. It must meet specific standards for use and “purity” guidelines for collecting.

It’s extremely difficult to produce and becoming more and more scarce…

Meanwhile, perhaps the biggest argument against gold out there is that historically, governments have actually banned the storage of gold… or made it inconvenient to own. Others have gone as far as confiscating it.

In 2010, gold bugs lost their minds after discovering a hidden gold tax buried in the Obamacare legislation, whereby coin and bullion transactions over $600 in a calendar year and made by small businesses and self-employed people were reportable.

But that seems relatively innocuous when you consider the fact that it was actually a federal felony to own gold in the U.S. from 1933-1974, unless you had a special license.

In fact, it was one of Franklin D. Roosevelt’s first acts as president. In the midst of the Great Depression, Roosevelt wanted to stop Americans from withdrawing their gold and currency from the wrecked banking system. So he ordered all banks to shut down from March 6-9th, 1933, "in order to prevent the export, hoarding, or earmarking of gold or silver coin or bullion or currency."

But it wasn’t enough.

Fearful of Americans draining the system, one month later, Roosevelt issued Executive Order 6102 and made outright gold ownership illegal — both in coins and in bars. If caught and prosecuted, owning gold was subject to up to 10 years in prison and a fine of “twice the amount of gold that was not turned over to the Federal Reserve in exchange for paper money.”

And even if all of that doesn’t dissuade you from being a nut about owning gold…

On top of it all, gold is just… not a good long-term investment.

Gold's Subpar Investment Performance

On DIYwealth.com, we often make fun of traders and retail investors because they often get a miserable long-term return on their investments because they simply… do too much.

The average stock investor gets something like a 3% to 4% annualized return.

That’s barely better than inflation…

And you know what? Gold is hardly any better.

Since 1980, the average annual return for gold was 3% (not adjusting for inflation).

And bear in mind: gold is a speculative asset.

Whenever you buy gold, you buy it hoping that some future schmuck is going to pay you more than what you bought it for.

It’s not like a bond that pays you fixed income or a business that generates products and shares profits…

Gold is, I reiterate, a shiny rock. Valuable only due to perception.

Now let me ask you this: When you think about investing your money, getting rich, saving for retirement…

Does it excite you to risk your money on something that has historically generated returns barely better than inflation?

Probably not.

So that’s the case against gold, and why we don’t recommend gold or precious metals as a proper “investment,” per se.

And yet…

With sky-high inflation and the prospects of a global recession looming, there might be a good reason to be bullish on gold and precious metals generally…

Why Gold Looks Like an Appealing Speculation in 2023

Let’s quickly revisit what happened in 2022…

To combat out-of-control inflation, the U.S. Federal Reserve Bank initiated two policies: rapid interest rate hikes (to make debt more expensive and discourage growth) and quantitative tightening (to get rid of some of the Fed’s bond and mortgage-backed security holdings, removing some of the support they provided to the stock and bond markets).

This is why, in 2022, we saw the rare phenomenon of both the stock and bond markets crashing.

After all that, it finally looks like inflation is starting to come down in 2023.

(If you’ve been following our blog, you already knew this would happen. I’ve been predicting a sudden and unexpected reversal in 2023 inflation for several months now. Check out my research and proprietary inflation models here.)

Also while the U.S. economy continues to grow, there are many signs that the Fed monetary policies are beginning to have their intended effect.

This led to a small surge in stock prices at the beginning of 2023.

But will this temporary bull market hold? And how does this all affect today’s asset focus: gold?

This gets a bit weedsy, but stay with me…

Reason No. 1 to be Bullish on Gold in 2023: The Death of the Dollar

The first and most important effect of the Fed’s efforts is that it massively increased the yield on short-term U.S. treasuries.

This has caused a global investment flight to U.S. denominated bonds, resulting in the U.S. Dollar gaining against almost all other currencies in the world. You can see that in the U.S. Dollar Index, which gained 8.18% in 2022.

It is hard to believe that, in 2022, one of the best assets to have held was simply cash. But it was a strange year with unusual circumstances.

But now, two new things are happening that are threatening to topple the dollar’s dominance…

First, other nations’ central banks are rapidly trying to “catch up” to the U.S.’s rate hikes. Most nations are doing what the U.S. began over a year ago. Now international investors and banks do not have to “flee” to dollars. (I’ll explain what this means for gold in a moment.)

Second, the U.S. looks highly likely to enter an economic recession in late 2023 or 2024.

There are a variety of reasons for this. But I like how analysts from the enormous asset management firm BlackRock stated it:

Recession is foretold as central banks race to try to tame inflation. It's the opposite of past recessions. Central bankers won't ride to the rescue when growth slows in this new regime, contrary to what investors have come to expect. Equity valuations don't yet reflect the damage ahead.

Translation: Basically, analysts from BlackRock suspect that central banks will not be quick to rescue markets and economies in the event of a recession or crash. This will make a long, painful recession inevitable as high rates prevent growth (and inflation) for the sake of stability.

Personally, I find BlackRock’s analysis to be a little too pessimistic considering that central bankers in the E.U. and Switzerland have literally said that they plan to “ride to the rescue” in the event of a calamity.

But also, I admit that I do not know everything. Nobody does.

So we must prepare for all eventualities.

What I do know is this: Signs are strongly pointing toward there being a recession in late 2023 or 2024… and further devaluation of the dollar.

So how will investors prepare for this double dollar destruction?

Well, now we return to where we started…

Gold.

Gold is the one asset that’s often recommended as a hedge both against a declining dollar and against a possible recession…

As of late 2022, gold was moving in the exact opposite direction as the dollar — gaining value at nearly the same pace the dollar loses value.

The escape from dollars to gold has already begun.

But is this trend likely to continue, and will gold really protect us from recessions?

The answer is “Yes, but it is complicated.”

Reason No. 2 to be Bullish on Gold in 2023: Recession Hedging

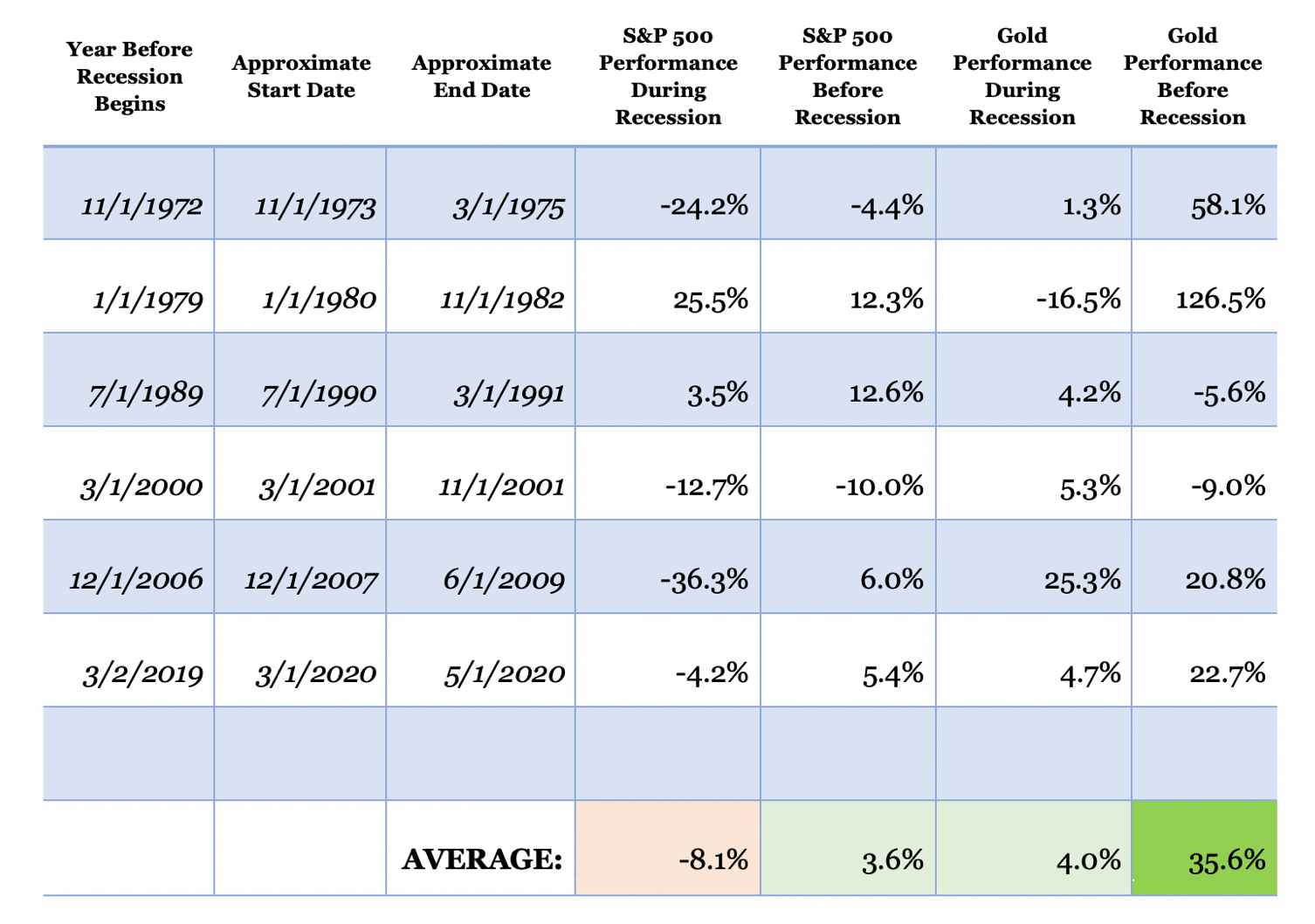

Since 1970, there have been seven major recessions in the U.S.

I looked at how the stock market did during recessions, and how the market performed in the year before a recession.

Here’s what I discovered:

We can make a few conclusions from these data.

For one, stocks are extremely risky to hold during a recession. That’s obvious.

The stock market (the S&P 500 in particular), dropped an average of -8.1% during recessions.

But less obvious is the fact that stocks are neutral-to-positive in the leadup to a recession, with some years gaining an above-average amount and some years losing.

Gold, on the other hand, performed pretty well during recessions, but performed amazingly well in the year leading up to a recession.

The belief that gold is a good “recession hedge” holds true, with gold increasing in value during all but one of the recessions over the last 50 years.

But in the year leading up to a recession?

It seems that investors know to buy lots of gold before the onset of a recession, which spikes the price.

That means that the best time to buy gold as a “recession hedge” is not at the beginning of a recession…

No.

The best time to buy gold as a “recession hedge” is long before a recession begins. Up to a year or more.

And guess what?

The best indicator that a recession is going to happen in the future, the yield curve, is telling us to expect a recession to begin in the next 6 to 18 months from time of writing.

To put it simply, gold looks like an attractive, smart speculation.

Something worth buying and holding — potentially for the next couple of years.

However, if you’re going to do this, the time to buy gold, if you want to protect yourself from a recession, is now.

Right now.

I personally just bought a few thousand dollars’ worth of gold and silver. If you want a shiny rock that tends to gain a lot of value before a recession begins? Consider doing the same.

How to Invest in Physical Gold, Silver, and Other Precious Metals

If you want physical, tangible, portable gold to hang onto in the coming years?

Grab some bullion if you can.

Gold bullion is gold in the form of bars, ingots, or coins.

In terms of purity, gold bullion can be 22 karats (91.7% gold) or 24 karats (99.9% gold).

The value of gold bullion generally tracks the spot price of gold, plus a “premium” (additional charge) that covers the cost of minting, storage, distribution, and sales commission.

The spot price is what it costs to buy at any given minute. It goes up and down, like virtually every commodity, due to speculation in the markets, currency values, current events, and other factors.

Although the spot price is very exact (down to the penny) and tracked to the second, it is a theoretical number in the sense that it represents the cost of gold without a premium. And there is almost always a premium, even between dealers.

Still, it is a very useful metric because it tells you, as a buyer, how much of a premium you are paying for the coins you buy.

So, then, what is a gold bullion coin? It’s a coin made by a private or public mint that is either 22 or 24 karats. Bullion coins are usually distinguished from numismatic coins. (Numismatic coins are limited in supply and bought for its rarity and beauty, like fine art. Rare coins can make good investments.)

If you want to buy online? You can buy gold bars from dealers, individuals or online from sites like JMBullion, the American Precious Metals Exchange (APMEX) or SD Bullion. (These are not affiliate links. We receive no compensation if you click or purchase through these dealers.)

Check out our comprehensive FAQ at the end of this article for specific recommendations of physical gold bullion coins to invest in.

How to Invest in Gold, Silver, and Other Precious Metals Using Your Brokerage Account

We just covered the ways to physically hold gold itself. And while you can definitely make money if gold prices rise, you won't be making any more money besides said capital gains.

Again, you can buy gold bars and bullion coins from dealers, individuals, or online from sites like JMBullion, the American Precious Metals Exchange (APMEX) or SD Bullion.

In contrast, investing in a gold exchange-traded-fund (ETF) may be another approach to consider.

ETFs are a broad, diversified basket of financial assets, such as stocks or bonds, that investors can buy.

By buying a gold-based ETF — such as the VanEck's Junior Gold Miners ETF — you'll have broad access to the gold market.

There are also different gold ETFs that focus on different aspects of the gold industry (junior miners, senior miners, etc).

In the issue of the Living Rich Monthly published in December 2022, I recommend my favorite gold-related stock that overcomes a lot of the problems the “anti-gold” camp has. Stay tuned in those pages for future gold-based recommendations.

Our Recommended Gold and Precious Metals ETFs

Frequently Asked Questions (FAQ) About Buying Gold

To answer all the questions we get on gold, we put together the following Q&A. It’s meant for tyros, but there may be information here that will surprise experienced coin buyers.

Q: What is Gold Bullion?

A: Gold bullion is gold in the form of bars, ingots, or coins. In terms of purity, gold bullion can be 22 karats (91.7% gold) or 24 karats (99.9% gold). The value of gold bullion generally tracks the spot price of gold, plus a “premium” (additional charge) that covers the cost of minting, storage, distribution, and sales commission.

Q: What is the "spot price" of gold?

A: The spot price is what it costs to buy at any given minute. It goes up and down, like virtually every commodity, due to speculation in the markets, currency values, current events, and other factors. Although the spot price is very exact (down to the penny) and tracked to the second, it is a theoretical number in the sense that it represents the cost of gold without a premium. And there is almost always a premium, even between dealers. Still, it is a very useful metric because it tells you, as a buyer, how much of a premium you are paying for the coins you buy. You can find the spot price of gold today right here from Kitco.

Q: What is a gold bullion coin?

A: It is a coin made by a private or public mint that is either 22 or 24 karats. Bullion coins are usually distinguished from numismatic coins.

Q: What is a numismatic or "collectible" coin?

A: It is a coin that is limited in supply and bought for its rarity and beauty, like fine art. Rare coins can make good investments. What I like about rare coins is that if you buy a bad one — a common coin in poor condition — it will still be worth at least the spot price of gold. But if you buy a truly rare coin in mint condition, it can eventually have a value that is 10 to 100 times the spot price of gold.

Q: Bullion coins vs. Numismatic coins: Which type should I buy?

A: If you are buying gold coins as a hedge against inflation or as insurance against the collapse of the dollar, you should definitely buy bullion coins, not numismatics. If you are buying gold coins as an investment, you should consider numismatics. You can, of course, buy both kinds of coins — at a ratio of maybe 60/40 or 80/20 bullion to numismatics. If you do buy rare coins, it is very important to buy from a trusted source. (See more on that at the end.)

Q: Are there different kinds of bullion coins?

A: Yes, there are hundreds — probably thousands — of unique bullion coins. But for beginners, it’s smart to group them in two categories: those minted by governments and those minted by private companies.

Q: So which kind of gold bullion coins should I buy?

A: For beginners… government-minted bullion coins — for several reasons: (1) They are minted in larger quantities, which makes them more liquid than privately minted coins. (2) The premiums (cost above the spot price of gold) are easy to track and therefore it’s easier to avoid overpaying for them. (3) They come with the inherent (and, in some cases, stated) backing of the government that mints them.

Q: Which government-minted coins do you recommend?

A: Most people buy bullion coins that are minted by the country they live in. Thus, most Americans buy the 1 oz. American Eagles (with Lady Liberty on the front and the American Eagle on the back) and American Buffalos.

Most Britons buy British Sovereigns. Most Canadians buy Canadian Maple Leafs. And many experienced coin buyers like South African Krugerrands.

Q: What are the differences between those three — the pros and cons?

A: The first difference is the purity of the gold. American Eagles and Krugerrands are 22 karat, which means they are about 92% (91.67%) pure gold. Canadian Maple Leafs and American Buffalos are 24 karat, which means they are 99.9% pure gold.

The second difference is the amount of gold. Maple Leafs and Buffalos are more pure, but Krugerrands and American Eagles are slightly bigger and weigh slightly more than their 24 karat cousins. That difference equalizes the difference. In other words, the amount of gold is the same (1 troy ounce) for all four coins.

The third and most important difference is the liquidity of a particular coin — how easy it is to buy and sell. Like every other asset class, the liquidity of gold coins depends on how many are available in a given market.

Of the four, American Eagles are by far the most liquid. About 80% of the gold bullion in circulation in the U.S. is in the form of the American Eagle. It is also the most-traded coin in the world. Krugerrands come in second. More than 50 million ounces of gold Krugerrands have been sold since production began in 1967. Maple Leafs come in third, with about 20 million in circulation. And Buffalos come in way behind with only about 2.5 million in circulation.

In terms of liquidity, I think Eagles, Krugerrands, and Maple Leafs are all a safe bet. Buffalos are safe, but I would not recommend them for beginners.

Q: Are there any other differences that I should be aware of?

A: There are a few that could be important.

Maple Leafs and Buffalos, being 24 karat, are softer than American Eagles and Krugerrands. That makes them more prone to bending and scratching. But condition is not a consideration in terms of tracking to the spot price of gold. They are all equal in this regard.

Another difference is the question of government backing as legal tender. As legal tender, the government that issues the coin guarantees that it can be used to settle a debt or meet a financial obligation. All four of these coins are guaranteed as legal tender.

Two final differences relate to investing and privacy. The American Eagle is an approved investment vehicle for Individual Retirement Accounts (IRAs). It is also exempt from the IRS’s Form 1099-B reporting requirements, which means your buys and sells are not publicly recorded.

The bottom line on these differences: All four of these coins are suitable as a chaos hedge and/or insurance against the collapse of the dollar, for example. In terms of gold content and government backing, all four are equal. The small circulation of the Buffalo puts it fourth on our personal preference list. And the IRA and privacy advantages of the American Eagle put it at the top.

Q: I heard that Krugerrands are illegal for U.S. citizens. Is that true?

A: No longer. They were banned in 1985 as a strategy to push South Africa to end Apartheid. The ban was lifted in 1991.

Q: Are there denominations of bullion coins like there are with dollars?

A: Yes. Eagles, Buffalos, Maple Leafs, and Krugerrands all come in four sizes: 1-ounce, 1/2-ounce, 1/4-ounce, and 1/10-ounce denominations.

Q: What denomination should I buy?

A: That depends on your budget and your purpose. In general, the smaller the denomination, the greater, in percentage terms, the premium. This is not unfair. Think of the premium as the cost of minting, storage, distribution, and sales. Those fixed costs are the same regardless of the size of the coin. So it stands to reason that the smaller coins will tend to have relatively higher premiums.

If your objective is to minimize the premium you will pay, you should buy the largest denomination you feel comfortable buying. However, there is an interesting argument for buying the smaller denominations: In a scenario of total economic collapse, gold (and silver) will become the currency of choice. In that situation, having smaller coins will make trading them for things that you need much easier.

Q: I’ve seen bullion coins. Some of them have dollar amounts printed on them. For example, the American Eagle has $50 on it. Does that mean the coin is really worth only $50?

A: Yes and no. What you’re looking at is the face value of the coins. In theory, face value is what the coin would be worth as legal tender. And if you were concerned about that, Krugerrands would be your choice since they have no face value and the South African government’s guarantee behind them is correlated to the spot price of gold. But in practice, the value of all bullion coins is correlated to the spot price.

Related anecdote: a banking teller acquaintance of mine once had a customer who came in to trade over a dozen (possibly stolen) American silver and gold eagles for their face value at the bank. The bank was happy to pay out the face value for the coins.

So if you’re really determined to trade in your $2,000 1 oz. gold eagle for $50 in cash, you will probably succeed. However, though this is not financial advice, we here at DIYwealth do not recommend doing this.

Q: Can I buy bullion coins directly from the U.S. and Canadian mints?

A: No. You have to buy them from a registered, private dealer — and each government publishes a list of those dealers. There was a time when you could buy American bullion coins from U.S. banks, but that is no longer true.

Q: What about dealers that sell online? Is it safe to buy from them? Or is it better to go with a local dealer?

A: It is usually just as safe to buy from a well-established dealer online (or by phone) as it is to buy directly from a local dealer — and there are some distinct advantages.

When you buy directly, you get immediate possession, you have no shipping or insurance fees, and you have more privacy.

On the other hand, the selection is likely to be more limited than it is with an online dealer. Plus, the price you pay will usually be slightly higher (because of the extra costs involved in retail business) and liquidity will be less for large buybacks.

Q: What about the coins that I see advertised on TV and in newspapers. Are those dealers safe sources?

A: Sometimes yes. Sometimes no. But considering the cost of that sort of advertising, the possibility of paying more than you should is something to consider. So long as you compare the price of the coin to the spot price of gold, you can figure out if you are being overcharged.

A problem with some of these dealers is that they have very persuasive salespeople that will try to get you to buy other types of gold coins with prices that are much higher than the spot price. The bottom line in buying gold bullion coins is the premium: how much the dealer is charging you above the spot price. Know the spot price. Demand a fair premium.

Q: Should high prices dissuade me from buying coins?

A: No. If you think of gold as an inflation hedge and/or as insurance against economic Armageddon, the one-time premiums you pay for almost any other form of insurance are comparable and sometimes higher.

If you are buying bullion coins for investment purposes, a premium of 6% or 10% is relatively high. It means that the spot price for gold will have to go up $120 to $200 an ounce before you make your first percent of profit.

Of course, if the spot price of gold goes to $10,000, current prices and premiums will seem cheap.

If you do decide to buy bullion for investment purposes, consider this: Krugerrands or Maple Leafs have, on average, premiums that are significantly lower than Eagles.

If, instead of paying a $120 premium for a 1-ounce Eagle you could buy a 1-ounce Krugerrand or Maple Leaf for a premium of only $80, why wouldn’t you do it?